- Blog

- Research & Reports

- New Delhi

The Parents' Veto Index 2026: India's First Dual-Lens Study on Parental Influence in Home Buying

Robin Gangawane

Robin Gangawane

- 2026-04-01 12:37:29

- 1200

- 0

Never miss any update

Join our WhatsApp Channel

The Parents' Veto Index 2026: How Indian Parents Add Rs.23.4 Lakh to Their Children's Home Purchases and Reshape India's Rs.585 Billion Real Estate Market

Published by Ghar.tv | March 2026 | 1,247 homebuyers surveyed | 12 cities | Consumer behaviour + Market economics

Executive Summary

As the average ticket size for housing in India's top cities crosses the ₹1.47 crore threshold in 2026, a powerful non-market force increasingly shapes transaction outcomes: the Parents' Veto. When a young professional buys a home in India, the de-facto investment committee almost always includes parents — either funding the down payment, providing full capital, or exercising cultural authority over the final decision.

This report is the first to quantify this phenomenon from two angles simultaneously: a primary consumer survey of 1,247 homebuyers revealing the emotional and financial cost of parental influence, and a market economics lens examining how parental priorities are reshaping demand across city tiers. For buyers navigating this process, our guide on 10 common mistakes to avoid as a first-time home buyer is an essential starting point — particularly relevant when multiple decision-makers are involved.

Four headline findings:

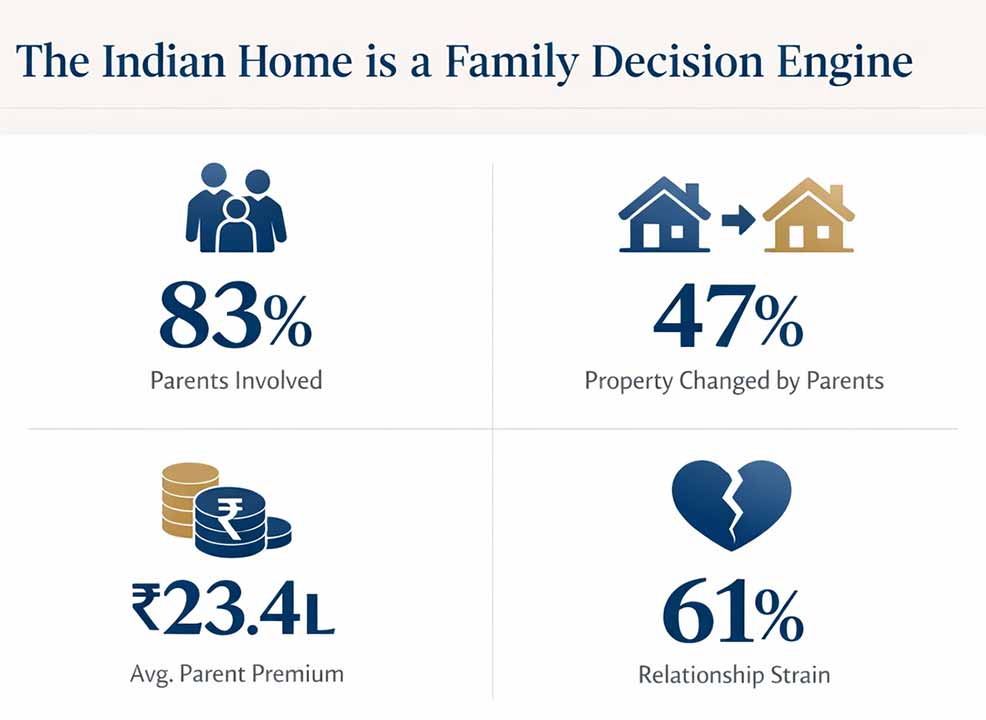

- 83% of Indian homebuyers say parents were meaningfully involved in their purchase decision

- 47% say the final property was materially different from their own first choice - due to parental pressure

- ₹23.4 lakh - the national average "Parent Premium" - additional spend above the buyer's own preference to satisfy parents

- 61% report moderate-to-severe relationship strain during the home buying process

"We had found the perfect flat in Bandra East. 2BHK, 7th floor, great light. Papa rejected it in 45 seconds because it faced west." - Software engineer, 33, Mumbai

Section 1: The Scale of Parental Involvement

How Involved Are Parents - Really?

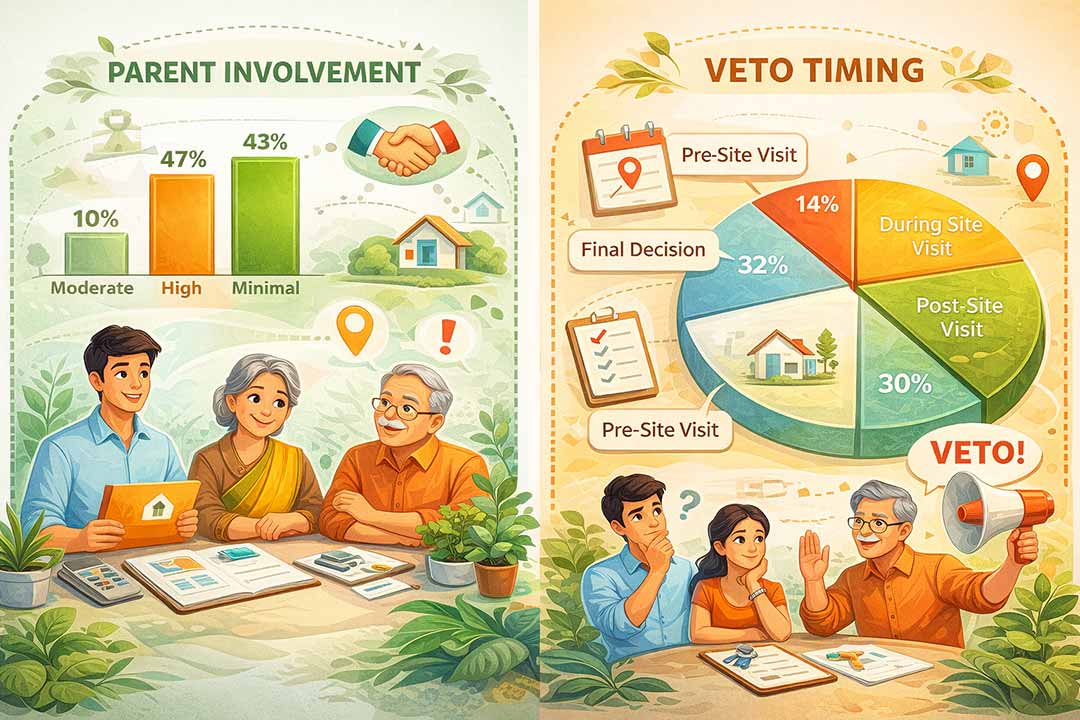

- Made the final decision: 19% (most common in Delhi-NCR, Jaipur, Lucknow)

- Heavily involved - significant veto power: 28% (Mumbai, Pune, Kolkata)

- Moderately involved - preferences considered: 36% (all cities)

- Slightly involved - consulted but not deciding: 12% (Bengaluru, Hyderabad)

- Not involved at all: 5% (Bengaluru tech professionals)

Whose Parents?

- Buyer's own parents: 58%

- In-laws (spouse's parents): 29%

- Both equally: 13%

Among married female respondents, 44% cited in-laws as the primary influencing party - vs just 18% of married male respondents.

When Does the Veto Land?

- Before search begins (set criteria upfront): 22%

- During shortlisting (eliminated options): 31%

- After site visit (rejected after seeing property): 27%

- After token booking — forced exit or renegotiation: 14%

- After agreement / during registration: 6%

"We had already paid ₹2 lakhs as token. My mother-in-law visited and said the kitchen faces north. We lost the booking amount." - IT professional, 37, Pune

Section 2: The Parent Premium

The Parent Premium is the measurable additional cost incurred by buyers who adjusted their property choice to satisfy parental preferences. Calculated from a sub-sample of 683 respondents. National average: ₹23.4 lakh, equivalent to 2.3 years of median EMI repayments. For buyers struggling with the financial burden of this premium, understanding why a longer home loan tenure can ease your EMI burden is worth considering early in the planning process.

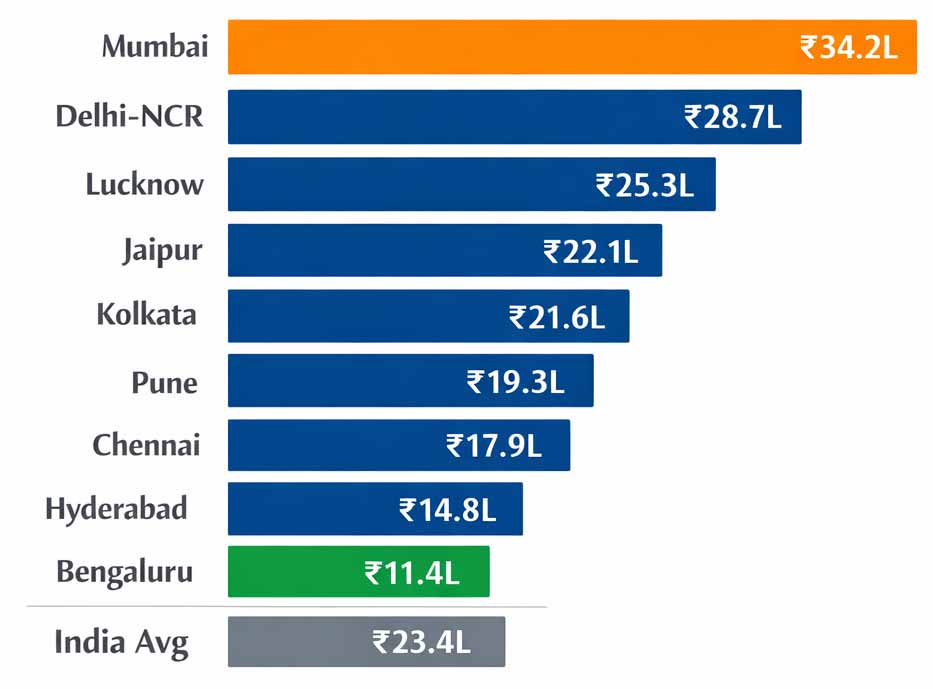

| City | Avg. Price (₹/sq ft) | Rental Yield | Parent Premium | Premium as % of avg. ₹85L home |

|---|---|---|---|---|

| Mumbai (MMR) | ₹18,000–25,000+ | 2.0–2.5% | ₹34.2L | 40% |

| Delhi-NCR | ₹6,000–11,000 | 2.0–3.0% | ₹28.7L | 34% |

| Lucknow | ₹4,500–6,500 | 3.0–4.0% | ₹25.3L | 50% |

| Jaipur | ₹5,000–7,000 | 2.5–3.5% | ₹22.1L | 44% |

| Kolkata | ₹5,500–8,000 | 2.5–3.0% | ₹21.6L | 43% |

| Pune | ₹6,500–9,000 | 2.5–3.5% | ₹19.3L | 23% |

| Chennai | ₹7,000–10,000 | 2.5–3.5% | ₹17.9L | 21% |

| Hyderabad | ₹7,500–11,000 | 3.0–4.1% | ₹14.8L | 17% |

| Bengaluru | ₹8,000–12,500 | 3.0–4.1% | ₹11.4L | 13% |

| National Average | - | - | ₹23.4L | - |

Hidden Costs Beyond Purchase Price

- Longer commute (fuel + time, 10-year equivalent): ₹9.2L - affects 67%

- Interior redesign to meet parental preferences: ₹3.8L - affects 44%

- Cancelled bookings / token money lost: ₹1.1L avg. - affects 14%

- Legal / second opinion costs on builder: ₹45,000 - affects 22%

- Pandit / Vastu consultant fees: ₹22,000 - affects 58%

Section 3: The Veto List - What Parents Actually Reject

Top 12 parental veto triggers (multiple selections allowed):

- "Too far from our home / relatives" - 72%

- "Wrong Vastu - bad direction or facing" - 61%

- "Builder not reputable / not heard of them" - 54%

- "Flat is on an unlucky floor / floor number" - 49%

- "Society is too modern / open plan" - 43%

- "Not enough space for guests / puja room" - 41%

- "Area has 'wrong' community mix" - 38%

- "Too close to a hospital / cremation ground" - 36%

- "Previous owner had bad luck / death" - 29%

- "Not enough natural light for puja" - 27%

- "Road-facing property - bad for energy" - 24%

- "Top floor - not safe during earthquake" - 21%

The Vastu Veto by City

Vastu compliance is one of the most decisive and least negotiable, parental criteria. Understanding the specifics can save buyers enormous time and money. Our comprehensive guide to 20 powerful Vastu tips for bringing positive energy into your home covers the most common parental concerns, and our dedicated resource on best house-facing directions in India according to Vastu Shastra addresses the single most frequent rejection trigger.

| City | Vastu Veto Rate | Primary Concern |

|---|---|---|

| Chennai | 78% | Kitchen direction - east-facing required |

| Ahmedabad | 74% | Main door facing - north or east only |

| Jaipur | 71% | Staircase location and direction |

| Mumbai | 62% | Master bedroom in southwest quadrant |

| Pune | 59% | Toilet placement relative to puja room |

| Delhi-NCR | 52% | Open plot / irregular-shaped land |

| Kolkata | 44% | Mixed - varies by community |

| Bengaluru | 29% | Lowest - most buyers dismissive |

For those wanting to understand Vastu room by room, our toilet and bathroom Vastu tips for modern homes and our complete guide to north-facing house Vastu in 2025 are among the most referenced resources on the topic.

The Floor Number Taboo (49% of Vetoes)

- Ground floor preferred: South India, elderly parents

- 13th floor avoided: pan-India

- High floors (8+) rejected: earthquake anxiety - Kolkata, Delhi-NCR

- Odd-numbered floors preferred: some communities in Gujarat, Rajasthan

- Floors ending in '4' avoided: Chinese-Indian heritage communities, Kolkata

Ghar.tv proprietary finding: Units on the 13th floor sold at a 6.3% discount to identical units on the 12th or 14th floor of the same building.

"My parents hired a Vastu expert at ₹18,000 who walked through the flat, checked his compass, and rejected it. The builder was furious. We lost our preferred unit." - Finance professional, 31, Chennai

Section 4: The PVI City Index - Consumer Behaviour Meets Market Reality

PVI Score (0–100): composite of involvement frequency, property alteration rate, and Parent Premium relative to city median price. 100 = maximum parental control.

| City | PVI Score | Category | Price/sq ft | Rental Yield | Key Note |

|---|---|---|---|---|---|

| Jaipur | 91 | EXTREME | ₹5,000-7,000 | 2.5-3.5% | Family proximity + RERA compliance |

| Lucknow | 88 | EXTREME | ₹4,500-6,500 | 3.0-4.0% | IT + Metro catalyst |

| Delhi-NCR | 82 | HIGH | ₹6,000-11,000 | 2.0-3.0% | Air quality concern |

| Kolkata | 79 | HIGH | ₹5,500-8,000 | 2.5-3.0% | Community mix driver |

| Mumbai (MMR) | 74 | HIGH | ₹18,000-25,000+ | 2.0-2.5% | Unmatched capital safety |

| Chennai | 71 | HIGH | ₹7,000-10,000 | 2.5-3.5% | Vastu rate 78% |

| Pune | 63 | MODERATE | ₹6,500-9,000 | 2.5-3.5% | Lifestyle balance |

| Hyderabad | 52 | MODERATE | ₹7,500-11,000 | 3.0-4.1% | No. 1 liveability 2026 |

| Surat | 44 | LOW | ₹5,500-7,500 | 2.5-3.5% | Builder familiarity |

| Bengaluru | 31 | LOW | ₹8,000–12,500 | 3.0-4.1% | Most independent buyers |

The Hyderabad sweet spot: PVI 52 (lowest among large metros) + rental yield 3–4.1% + India's No. 1 liveability ranking in 2026. The rare market where parental instinct and financial fundamentals align. Gachibowli and HITEC City represent the epicentres of this convergence, combining strong end-user demand with robust rental income from the tech professional segment.

Tier-2 Cities - Where Parental Capital Is Shifting

| City | Price/sq ft | Key Parental Attraction | Economic Catalyst | Value vs Bengaluru |

|---|---|---|---|---|

| Lucknow | ₹4,500-6,500 | Affordability, metro | IT and Defence | ~45% cheaper |

| Indore | ₹4,000-6,000 | Cleanliness, planned infra | Pharma and Auto | ~50% cheaper |

| Jaipur | ₹5,000-7,000 | Cultural hub, RERA | Tourism and IT/ITES | ~40% cheaper |

| Surat | ₹5,500-7,500 | Smart city infra | Diamond and Textiles | ~38% cheaper |

| Kochi | ₹6,000-8,000 | Coastal, modern lifestyle | Port, IT and Tourism | ~35% cheaper |

| Coimbatore | ₹5,000-7,000 | Healthcare and education | Textiles and Manufacturing | ~42% cheaper |

An investor can acquire assets in Lucknow or Indore at 40–50% of the capital outlay required in Hyderabad for a comparable property - while still benefiting from strong economic fundamentals and infrastructure-led growth. Our dedicated analysis of what makes property investment in Lucknow noteworthy explains why this city consistently outperforms expectations. Similarly, the evolution of Jaipur real estate and why Kochi is becoming a hotspot for realty investors illustrate how these markets have matured.

The WhatsApp Veto

34% of buyers with NRI family members report a property being rejected remotely via photos, video calls, and WhatsApp without the parent ever visiting.

- Parents added to property shortlist WhatsApp groups: 61%

- Final decision required parent's video call tour: 44%

- Property rejected based on photos alone: 38%

- Astrologer consulted remotely before decision: 27%

- Parent hired local "representative" to visit: 19%

"In Jaipur, not buying near your family is a statement. You're telling them you're not coming back. Property selection is a social negotiation, not a financial one." - Real estate developer, Jaipur

Section 5: The Gender Dimension

| Metric | Married Women | Married Men | Single Women | Single Men |

|---|---|---|---|---|

| In-laws as primary influencer | 44% | 18% | N/A | N/A |

| Property changed due to pressure | 61% | 39% | 28% | 21% |

| Reported relationship strain | 74% | 52% | 31% | 19% |

| Average Parent Premium paid | ₹27.1L | ₹21.3L | ₹14.2L | ₹11.8L |

| "I would have chosen differently" | 68% | 43% | 54% | 32% |

"My name is not on the property. My salary paid for it. My in-laws chose it. I live in it." - Schoolteacher, 34, Delhi-NCR

Single women buyers face unique pressures:

- 68% say parents insisted on a gated community over their preferred independent house

- 54% say parents' security concerns overrode their location preference

- 41% say parents delayed the purchase by an average of 14 months, urging them to "wait and see"

- 29% say parents suggested buying near a relative rather than near their workplace

Section 6: The Emotional and Relational Cost

- 61% report moderate-to-severe relationship strain during home purchase

- 23% seriously considered abandoning the purchase due to family conflict

- 17% say the purchase caused a lasting deterioration in a family relationship

- 8% still resent the property they live in because it wasn't their choice

Relationship Strain by Party

- Between spouses / partners: 58%

- Between buyer and in-laws: 52%

- Between buyer and own parents: 39%

- Between the two sets of parents: 31%

- Among siblings (inheritance concerns): 21%

"My wife and I didn't speak properly for three weeks. Not because of the property. Because of what choosing it meant - that her parents' opinions mattered more than mine." - Finance manager, 36, Mumbai

Regret Data - Four Years After Purchase

- No regrets - parents were right: 34%

- Minor regrets - would do 90% the same: 21%

- Significant regrets - wish I'd held firmer: 31%

- Deep regrets - actively planning to sell and move: 14%

45% of buyers who deferred to parental pressure wish they had held firmer. For those in the 14% considering a sale, our complete guide to selling your flat in 2025 - expert tips and strategies provides a practical roadmap for exiting and upgrading.

Section 7: The Silver Lining - When Parents Add Value

| Area of Input | % Who Said Parents Were Right in Hindsight |

|---|---|

| Builder reputation check | 79% |

| Resale value instinct | 71% |

| Structural quality concerns | 68% |

| Legal / title due diligence | 64% |

| Location proximity to family | 62% |

| Negotiation on price | 58% |

| Vastu compliance | 31% |

| Floor number preference | 24% |

The data tells a nuanced story: parental involvement on practical due diligence - builder track record, title verification, resale value - is broadly vindicated. The risk of chronic project delays is a real concern that parental caution about builder reputation directly addresses. Equally, the advantages and disadvantages of investing in a resale property - an area where parents often have superior instinct — deserves careful buyer consideration.

"My father insisted we verify the builder's past projects. I thought he was being paranoid. The builder had delayed his previous project by 4 years. We walked away. That flat is still unregistered today." - Doctor, 38, Hyderabad

Section 8: What the Parents' Veto Means for Investors

Institutional investment in Indian real estate surpassed ₹63,000 crore in 2025. Foreign PE investments reached approximately $3.1 billion in FY25. The trend signals a clear market shift towards properties that guarantee long-term value, larger unit configurations (3BHK+), and integrated townships with schools and clinics. For a macro view of this shift, India's big investment shift into real estate in 2025 provides essential context.

Investor Strategy Matrix

HNI (Capital Growth)

Strategy: Well-connected micro-markets in high-liveability Tier-1 cities. Target markets: Hyderabad (Gachibowli, HITEC City), Pune (Hinjewadi). Track: Price appreciation + infrastructure completion timelines.

NRI (Yield + Safety)

Strategy: High-yield corridors in established IT hubs with strong tenant demand. Target markets: Bengaluru (Sarjapur Road), Hyderabad (HITEC City) - 3-4.1% yields. Our guide on where NRIs should invest in India for top property growth maps these corridors in detail, while NRIs now account for 20% of India's property sales in 2025, a structural shift that is here to stay.

Family Office (Long-Term Hold)

Strategy: Diversify between stable Tier-1 and high-growth Tier-2. Target markets: Mumbai redevelopment (Andheri, Chembur) + Lucknow / Indore. The best real estate mutual funds in India for 2025 represent a complementary vehicle for family offices seeking blended exposure without direct property management obligations.

First-Time Family Buyer

Strategy: Integrated townships in affordable Tier-2 or peripheral Tier-1 suburbs. Target markets: Lucknow, Indore, Panvel (Navi Mumbai - now under 20 minutes to Sewri via MTHL). If financing is a concern, what to do if you've failed to get a home loan and how to find the right home loan easily are essential reads before approaching any lender.

Infrastructure Trust Signals Parents Respond to Most

- Metro connectivity (operational line): 68%

- Reputed hospital within 5km: 64%

- Top-5 school within 3km: 61%

- RERA-registered project with OC history: 58%

- Major highway / expressway access: 52%

- Smart City Mission designation: 41%

The RERA trust signal is particularly significant. Five years of RERA — how the law has changed Indian real estate shows how the regulatory framework has directly addressed the builder reputation veto that is the third most common parental rejection trigger. The wider shift to digital documentation is also helping — India's digital property revolution in 2025 and the new law to digitize property records and safeguard NRIs from scams are building exactly the institutional trust that converts a parental concern into a parental endorsement.

Section 9: Forward Outlook - 2026 to 2030

The influence of the Parents' Veto is set to intensify. As India's GDP approaches ₹613 lakh crore by 2030, the pool of parental capital available for real estate investment will expand significantly.

| Period | Market Size | Key Dynamics | HPI Growth Forecast |

|---|---|---|---|

| 2026- Now | $585 billion | Average ticket size crosses ₹1.47 crore in top cities. Tier-2 cities capturing growing share of family capital. | 6.5-7.5% |

| 2027-2028 | $700–750 billion | Smart Cities Mission completions in Lucknow, Indore, and Jaipur expand parental confidence in Tier-2 markets. | 5-6% |

| 2029-2030 | ~$926 billion | Generation Z enters home-buying age. REIT penetration expected to breach 20%. | 5-6% (sustained) |

The RBI's 50 BPS rate cut sparking a real estate investment boom further strengthens first-time buyer sentiment and expands the addressable buyer pool in the ₹50–85 lakh segment where parental capital is most active. Developers who successfully integrate the Veto parameters - safety, community, connectivity, and quality - into project design will command a significant market premium through 2030. The Parents' Veto is not a soft factor. It is a structural market force.

Section 10: Recommendations

For Buyers

- Define non-negotiables before starting the search - communicate them to parents before viewings begin, not after

- Separate evidence-based concerns from emotional preferences. Let parents own builder due diligence; you own commute and layout

- Do not take parents to first viewings - shortlist to 2–3 options alone, then involve family

- Budget for the Parent Premium explicitly - if parental involvement is likely, add 15-20% to your projected cost

- Use pricing data to have a factual conversation about Vastu and floor preferences - superstition has a measurable price. Our top Vastu tips for home decor can help frame these conversations constructively

For Developers and Brokers

- Never schedule multi-generational site visits unless the buyer explicitly requests it

- Build a parent pitch deck: RERA compliance, builder track record, OC history, resale data, hospital and school proximity

- Train sales staff to identify who in the room actually holds veto power

- Market Vastu compliance explicitly where genuine - it is a legitimate criterion for the majority of Indian buyers

- In Tier-2 markets, lead with infrastructure adjacency - it is the No. 1 parental trust signal

For Policymakers

- RERA compliance transparency directly addresses the builder reputation veto — most evidence-based and most easily solved by data

- Property title simplification reduces the legal anxiety driving parental control over transactions they don't fully trust

- Accelerating Smart Cities Mission delivery in Tier-2 cities unlocks the next wave of family capital formation outside Tier-1 metros

Methodology

- Sample: 1,247 homebuyers who completed a purchase in the 36 months prior to survey date

- Age: 24-45 years

- Cities: Mumbai, Delhi-NCR, Bengaluru, Hyderabad, Pune, Chennai, Kolkata, Ahmedabad, Jaipur, Lucknow, Chandigarh, Surat

- Method: Online survey (62%), in-person interviews (24%), telephone (14%)

- Property types: Residential apartment (81%), independent house/villa (13%), plot (6%)

- Gender: 53% male, 44% female, 3% non-binary / preferred not to say

- Marital status: Married (74%), unmarried (21%), divorced/separated (5%)

- Parent Premium sub-sample: 683 respondents who reported a significant property change due to parental influence

- Market data sources: Ghar.tv listing database, Cushman & Wakefield India Outlook 2026, Colliers India Office Outlook 2026, Mordor Intelligence

- PVI Score = composite of Involvement Frequency Index + Property Alteration Index + Parent Premium Index (equal weighting)

- Limitations: Self-reported financial estimates carry inherent bias. Study captures buyer perception of parental influence only. Rural markets not represented. Market price data reflects Q1 2026 averages.

About Ghar.tv

Ghar.tv is India's first media-led real estate ecosystem - combining an AI-powered property platform with original video content, market intelligence, and expert conversations. Founded 2022, headquartered in Mumbai.

Press: [email protected] | Research licensing: [email protected] | Platform: ghar.tv

Copyright 2026 Ghar.tv / Zybeq Ventures Pvt. Ltd. May be cited with attribution. Full reproduction requires written permission.

Comments

No comments yet.

Add Your Comment

Thank you, for commenting !!

Your comment is under moderation...

Keep reading blogs